Time for investors to look past worrying news flows

For investors, the news flow remains worrying – yet many risk assets flash long-term bottom signals. Investors should not forget that reality may differ from the headlines. In this Research Weekly, our experts explore growth in China, the eurozone, and the USA.

A word from Head of Research Christian Gattiker

As with the ‘No Future’ generation of the 1980s, the ‘Last Generation’ now also believes that the end is nigh. At the same time, there are strikes in many European countries, inflation is at staggering levels, and the Fed is performing ‘Volckeresque’ stunts in monetary policy. I would not be surprised to see Ronald Reagan coming round the corner hand in hand with Margaret Thatcher. Maybe they have already done so but have taken on more sanctimonious forms. And who coined ‘Inflation Reduction Act’ (IRA) for the programme designed to bring President Biden successfully through the US presidential elections in 2024? ‘Ira’ means ‘anger’ in Latin, and that is probably the least controversial political reference here.

All in all, the present situation feels like another twist in the ‘Back to the Future’ saga (part 4 was rumoured to be released this year). But then again, it may be comforting to relate back to the bad old days just to realise that the headlines may somehow hide reality. And even this storm may pass too.

Looking at recent data, one must admit that the world economy is doing rather well. The US is likely to print a +2% growth figure for the first quarter of this year. At the same time, the eurozone will likely avoid recession yet again. And China is showing economic strength after the reopening.

Our economists upgraded full-year growth forecasts there to +6%. So it may be for a reason, after all, that many risk assets are flashing long-term bottom signals according to technical analysis. And investors may simply want to show stamina against the pitch-black mood in many places. We stick to our theme of European banks distributing cash generously while trading at depressed valuation levels.

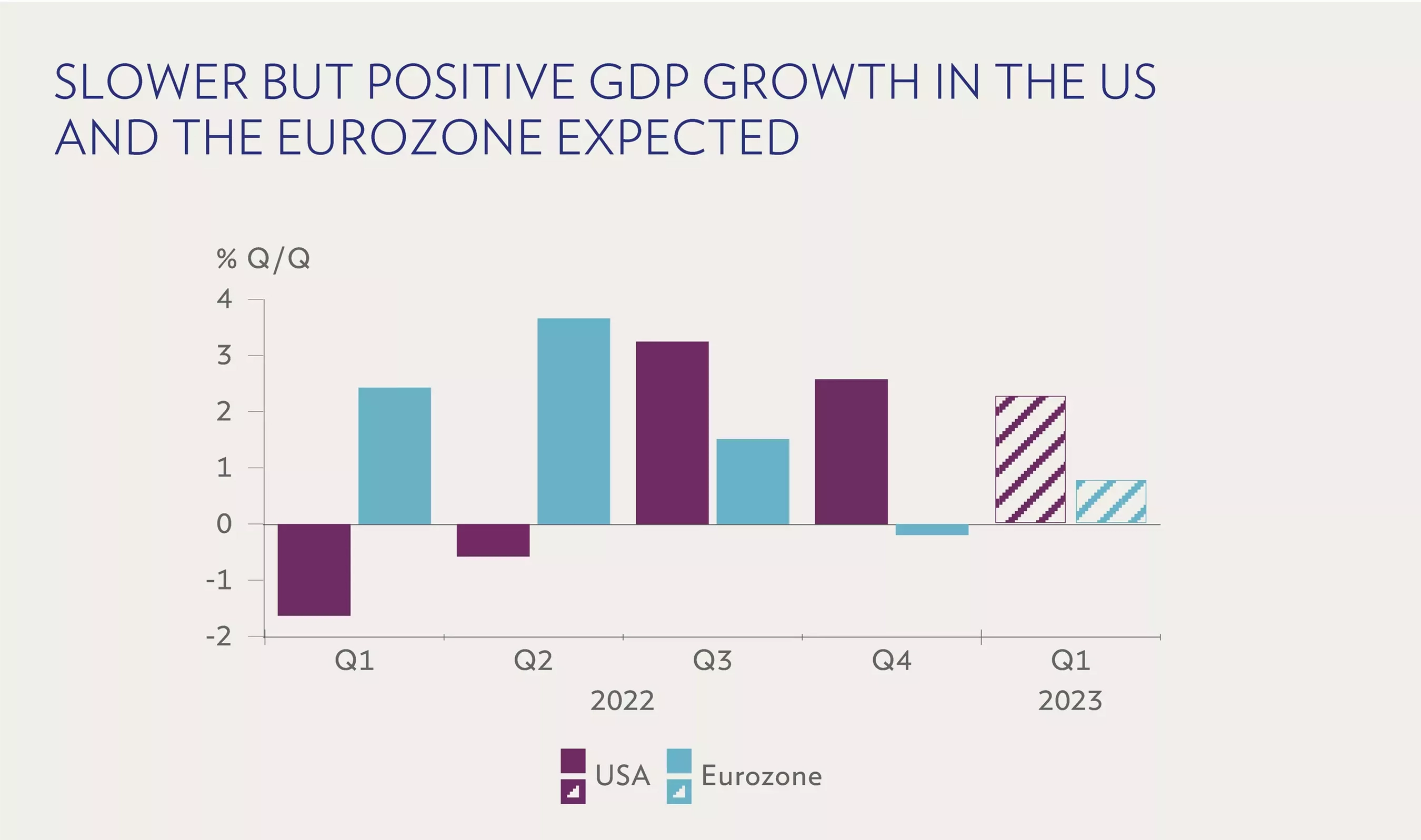

A word from our Chief Economist David Kohl

First-quarter GDP growth in the US and the eurozone is likely to have held up reasonably well. Expectations have adjusted in the past few months to the more sanguine view that a recession is not imminent despite the many shocks that have hit the economy. The war in Ukraine, a sharp rise in energy prices, high inflation rates, sharply higher interest rates, and corrections in equity markets have slowed economic activity, particularly in Europe.

At the same time, none of these shocks has triggered a self-feeding downward spiral in economic activity. We expect low but positive GDP growth in the eurozone and solid growth in the US.

Some of the main drivers of economic growth in the first quarter should continue to support growth in the future. We expect private consumption growth to have been an important driver, especially services consumption, given the high employment rate and excess savings. Both help to offset the drag from higher prices and depressed sentiment. The support from excess savings will fade as the year progresses. At the same time, even interest-sensitive growth drivers, such as investment in general and residential investment in particular, are holding up better than feared, given the limited capital-stock levels, which create strong investment needs.

We anticipate net export growth to play a more positive role in the eurozone than in the US and to benefit from the pickup in China. We expect growth to benefit from the current momentum in the first half of the year before slowing further in the second half.